A new IT revolution has arrived. New capabilities created by platforms based on cloud & big data – collectively referred to as data technology ─ are replacing support systems & traditional IT models.

Key takeaways:

- Data Technology – platforms based on big data and cloud – will become the new IT.

- Transforming data services and platforms inside-out enables operators to upgrade to

XaaS data services for core service scenarios.

- In the data transformation era, a new operator landscape is shaping up comprising four groups.

A new IT revolution has arrived. New capabilities created by platforms based on cloud & big data – collectively referred to as data technology ─ are replacing support systems & traditional IT models.

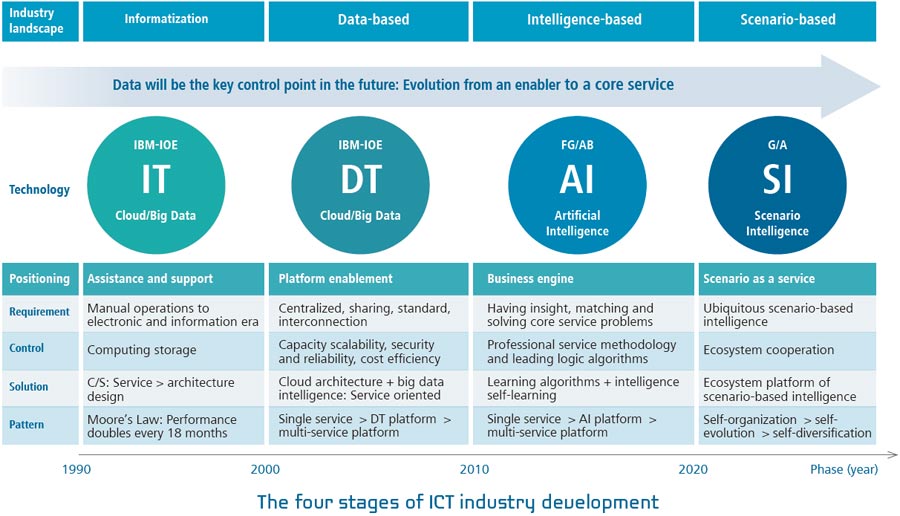

From IT to DT

Four stages of development exist for ICT: IT (support), DT (enabling), artificial intelligence (service), and scenario intelligence (intelligent).

During the 1980s and 1990s, the US transitioned from the analog to the digital IT era. Digital tech like computers, storage, and databases transformed society, with companies like IBM, Oracle, and Dell EMC as the pioneers.

The advent of IT saw a process of global horizontal integration led by IBM. The generalization of IT hardware coupled with the standardization of software led to compatible computers becoming standard across all industries, improving cost efficiency models across the board.

Analog society had gone digital.

Through its App Store and open APIs based on iOS, Apple has built an ecosystem of Internet-content apps that combine tech, art, and culture. This has created a stream of innovation in devices and service experiences, with the iOS-based vertical integration model of experience replacing the IT era’s horizontal integration model of efficiency.

It’s time to transition

Now, we’re quickly transitioning into the DT era, with cloud, big data, and smart technology at the helm.

Since 2000, the Internet has propelled innovation in cloud and big data innovation forward. The Internet provides far cheaper computing, storage, and service logic than traditional IT, bringing with it a much more agile service model that redefines what a platform is. In turn, DT has evolved from an auxiliary support system to a platform enabler and service engine.

New DevOps models have been developed for DT platforms to provide Internet services with a ROADS experience (Real-time, On-demand, All-online, DIY, and Social). Internet companies define DT as data-driven cloud, big data, and smart technologies, which is distinct from IT.

Since 2010, continual breakthroughs have been seen in intelligent data analytics and service innovations. In some areas, artificial narrow intelligence (or weak AI) like IBM's Deep Blue and Watson and Google's AlphaGo have already exceeded human capabilities in specific fields, laying the path for the possibility of artificial general intelligence.

Humanity will then enter the stage of scenario intelligence (SI), where all scenarios and industries are intelligence-driven.

Two types of integration

Like IT, DT will integrate in two ways: horizontally and vertically. Over three decades, we’re seeing three major trends.

1995-2005: IBM's horizontal integration delivers low-cost PCs. IBM developed the 286/386/586 series of PC-compatible computers that, when popularized, gave rise to global information sharing and the modernization of industry, forging a trillion-dollar IT industry that drove global development. Humanity entered the information age.

2005-2015: Apple's vertical integration innovates with experience. The iPhone and App Store spawned two million apps, creating the mobile Internet era and a new trillion-dollar industry. In this decade, humanity entered the mobile Internet age. Here, the stage was set for DT to replace and surpass inefficient, expensive IT, drive industrial digitization, and take us into the data-driven DT age.

2015-2025: Amazon's horizontal integration positions cost efficiency at the core. In Q3 2015, the number of AWS's business customers tripled over the short span of three years to hit 1 million, helping the company to finally start making profits. In this stage, the cost efficiency of cloud services will accelerate innovation, market segmentation, and data transformation for verticals. Horizontal integration will also gather speed.

Google's vertical integration results in specialization and intelligence: IBM's cognitive computer Watson, Google's AlphaGo, and government cloud transformation exemplify the start of vertical market integration, which is likely to peak in 2035.

DT-driven vertical integration and horizontal integration will be how industries develop in the future under a fully transformed device-pipe-cloud model. To survive, enterprises must find a place in this model and innovate.

DT's three major schools

Under the specialized and enabling ideal, DT transformation is divided into three schools: industry, over-the-top (OTT), and telecommunications.

Industry: The competitiveness of vertical integration depends on specialization

As well as horizontal integration, DT transformation will accelerate the vertical integration of industries. Industry leaders will apply DT as a general technology to make breakthroughs in their sector.

With Industry 4.0, for example, German companies such as Mercedes-Benz, BMW, and Bosch are making decisive moves into IoT, big data, and intelligent factory management, production, logistics, manufacturing processes, and other scenarios. Boosting production and technical capabilities and management efficiency by more than 50 percent, such data-driven strategies have strengthed the leadership position of each in their respective sectors.

OTT: DT-enabled competitiveness extends to general industries

Internet companies are using innovative data-based solutions to transform business models in industries like logistics, retail, finance, and banking, and becoming leaders as a result. Big-name examples are Google, Apple, Facebook, Amazon, Baidu, Alibaba, and Tencent.

However, these OTT companies are hindered by a lack of specialized know-how, preventing them from entering highly specialized sectors such as manufacturing and healthcare, despite attempting to do so with M&As. In these sectors, the current leaders must transform to quickly establish leadership in new areas.

Operators: Localization and integration are the way to go

Operators lack services and scenarios in horizontal integration for DT. Without a background in DT, incentivized cultures, or mechanisms for rapid iterative innovation, it’s tough to compete with OTT and vertical industry leaders.

The only option for operators is to provide customized vertical integration services for mid-level customers that have a greater need for localized resources. When it comes to horizontal and vertical integration, operators should adopt the models of OTTs and industry leaders and bundle and use local resources to provide data-driven customizable services at a local level.

How to transform

With big data and specialized services as the best starting points, service scenarios form the foundation for adopting DT. Operators' DT transformation strategies therefore require an inside-out model that first upgrades and transforms internal resources and service platforms (+ DT = IT 2.0) and then upgrades customers’ service platforms (DT + = DT 1.0).

In the data transformation era, a new operator landscape comprising four groups is taking shape around the world. The US, Japan, and South Korea are the leaders. Close behind is China with rapidly developing Internet and LTE networks. Europe has fallen behind, forming the third group. The fourth is made up of developing markets.

The US: AT&T is a typical example from the leading group when it comes to data transformation. In its core strategy Domain 2.0, AT&T has replaced access and carrier network hardware with commercial-off-the-shelf hardware and formed a Central Office Re-architected as a Datacenter (CORD) model with its data centers. It has cloudified control and operations management, making it smart and data-driven to form an ECOMP platform.

China: China Telecom's data transformation strategy sets out three cornerstones – making its networks smart, implementing operating intelligence, and creating a service ecosystem.

Europe: Telefonica's data strategy, Onlife Telco, outlines three horizontals – connectivity, enablement, and services – and two verticals: data and data-enabled capabilities.

Despite the different names, these strategies have the same architecture and apply the same methods: applying data to improve services and platforms.

+DT = IT 2.0

DT transforms networks, O&M, services, management, and process services under an inside-out model. Operators can take both a collaborative or competitive approach.

Collaborating: Telefonica and Amazon and China Unicom and Alibaba are examples of strategic collaboration on DT. The partners are building DT-driven operations, business, and management systems that are run in-house, aiming to engender data sovereignty coupled with fully internal DT-based operations and service capabilities.

Competing: To compete with OTT leaders' strategies, like Facebook's TIP strategy and Google's SDN and B4 strategies, AT&T quickly rolled out Domain 2.0 to transform its network into a DT platform for Internetized services. SDN/NFV, cloud, and data technology will minimize cost, support a ROADS experience, and enable Internet and service innovation.

Transforming data services and platforms inside-out enables operators to upgrade to XaaS data services for core service scenarios, enhancing DT-enabling services for primary service scenarios like data centers, CDN, cloud computing and storage, data analysis, and smart tools.

There are four main service scenarios that will help deliver profitable breakthroughs for operators:

Digital Shopping Mall (DSM): Localized innovation and collaboration are key here. KDDI's Smart Pass, DoCoMo's Smart Life, and Telefonica's aggregated pan-Hispanic content DSM are successful examples of DSM that compete well with OTT services such as Netflix, YouTube, App Store, and Google Play. Operator DSMs emulate the Apple's App Store model, but offer customized and localized services.

Fixed-mobile convergence (FMC) 2.0: BT, Sichuan Telecom, PCCW, and DirectTV (an AT&T acquisition) have all achieved success with FMC 2.0. In 2015, 17 carriers from the Global 500 implemented FMC 2.0, with the three fastest growing all providing FBB and video as core services. Explosive growth in video triggered by LTE has quickly shifted service scenarios to an FMC 2.0 model that includes broadband and video, presenting a great opportunity in the post-LTE market, especially as video requires data support platforms.

Enterprise E2E services: To use DT to meet enterprise needs for cost-efficiency, security, and reliability, AT&T provides Fortune 500 companies with services such as ubiquitous broadband access networking, 40-plus data centers, software and hardware security, enterprise-grade application proxies, and DevOps online data transformation support.

Industry DT strategy: Localized and customized, horizontal integration reaches 60 to 80 points in DT competitiveness based on cost efficiency indicators, while vertical integration DT scores 90 to 100 points.

Industry leaders will need to adopt a customized top-down model for DT transformation. Big names like Mercedes-Benz, Bosch, Huawei, and China Merchants Bank offer unique services and implement rapid iterative upgrades. They’ve all chosen to build vertical data-based platforms and service ecosystems, unlike small businesses, which must choose the most cost-effective horizontally integrated DT platforms. Operators have advantages in the medium enterprise market, particularly the government market, where customers expect high-grade service security, reliability, data sovereignty, and localized services.

With the demand for data sovereignty increasing across the globe, government clouds and other data-based services represent a key opportunity for operators over the next five years; for example, Deutsche Telekom is an early mover, providing localized government cloud services with data sovereignty protection and service security to the German government.

Every enterprise needs DT

As complementary forces for the data transformation that shifts IT to DT, horizontal integration creates cost efficiency, while vertical integration promotes specialization and smart operations.

Data transformation is user-inspired and service-oriented, with customer demand for an Internetized ROADS experience shaping platforms. Initially, operators will choose an inside-out transformation model that first targets their network, support, O&M, and service systems, and then provides platform-based services to other companies on a collaborative basis. There is also the fourth way of providing platform services for other companies: localization, customization, bundled infrastructure resources, and telecom-grade service protection.

However, one thing is clear: DT is the future and every enterprise must transform to embrace it.